A number of platform companies have been found guilty of false invoicing! Failure to actually organize and manage workers at issue

Editor's Note: In recent years, many enterprises have begun to reshape the original employment relationship through the unique mechanism of Internet platform enterprises (e.g., flexible employment platforms, network freight platforms, etc.), forming a new employment model of “laborer-platform-employer”. However, the reshaping of this employment model may cause the tax authorities to doubt the authenticity of the business and the legitimacy of the invoice. This article will combine two cases of platform enterprises suspected of false invoicing to analyze whether it is reasonable and legal for the tax authorities or judicial authorities to determine the invoices as false invoicing on the ground that “the platform did not organize its own personnel” when the business involved in the case is equipped with real labor services and there is no return flow of funds, and put forward corresponding opinions and countermeasures.

Ⅰ. The platform accepts laborers and drivers recommended by the employer to be recognized as false invoicing

(Ⅰ) Case 1: enterprises bring their own riders, flexible labor platform is recognized as false invoicing

Recently, Changzhou Taxation Bureau served a penalty decision letter to Enterprise A, which determined that all VAT invoices obtained by Company A from a flexible labor platform were falsely issued, and Company A was found to have evaded tax and imposed a fine of 50% of the VAT amount and additional deduction. It was found that Company A obtained 10 VAT special invoices from a flexible labor platform with a total of RMB900,000 in price and tax, and the invoice names included items such as delivery fee for logistics auxiliary services, marketing of modern services and information system services for information technology services, etc. Company A paid a total of RMB900,000 to the flexible labor platform, which then transferred more than RMB830,000 to the names of 14 natural persons designated by Company A.

The above penalty decision was based on the fact that, according to the information provided by Company A, the salary schedule and the screenshots of the system background information of the incumbents, it was confirmed that these riders were in fact employed by Company A, that a flexible labor platform did not organize its own personnel to provide labor services to Company A, and that the invoices in question were fraudulently issued.

(Ⅱ) Case 2: the enterprise brought its own drivers, network freight platform was found to be false invoicing

The VAT invoice obtained by Enterprise B from a network freight platform was characterized by the tax inspection bureau as false invoicing, involving a large amount of tax, and the network freight platform had been judicially dealt with, and the inspection bureau intended to transfer Company B to the public security authorities for processing. company B is a local freight forwarding enterprise operating in the transportation business, and due to the high cost of maintaining a fleet of vehicles, does not have its own vehicles, and employs individual drivers to undertake the actual transportation work. Due to the individual driver invoicing willingness is not high, in order to solve the problem of input, the company contacted the provincial network freight platform, so that the individual driver in the network freight platform after registration to take orders, and through the network freight platform for settlement. Since the network freight platform does not have real-time settlement function, the freight is usually paid to the network freight platform by Company B through bank transfer, the platform deducts a certain service fee, and then pays the freight according to the list of drivers and bank accounts provided by Company B. The freight is paid to Company B through the network freight platform.

Company B's transportation business was real, and the freight charges were transferred to the individual drivers who actually undertook the transportation business through the online freight platform, with no return of funds. However, the Audit Bureau considered that the individual drivers were contacted by Company B itself, and the business in question was not formed through the network freight transportation platform, which was inconsistent with the business substance of the network freight transportation platform, and the platform paid the freight charges to the individuals and their accounts provided by Company B, which was suspected of fund flow back. Therefore, the Tax Bureau determined that the VAT invoices obtained by Company B were falsely issued.

(Ⅲ) Summary: Tax and judicial authorities are becoming increasingly stringent in defining the obligations of platforms

In the above case, although the laborers and drivers really provided services for the enterprise and there was no return of funds, the tax authorities still determined that the VAT invoices issued by the platform were falsely invoiced, and the core reason for this was that the platform failed to independently organize and manage the personnel to provide services for the enterprise. In the previous cases of false invoicing by platform enterprises, there were often “false invoicing without goods” and “false invoicing with goods” accompanied by the return of funds, but the determination of these two cases shows that the tax and judicial authorities have become increasingly stringent in their supervision of platform enterprises, and the business model of the platform is also taken into consideration. The business model of the platform is also included in the scope of consideration. Under the high pressure of many parties, platform enterprises and their recipients will face higher tax risks.

Ⅱ. The focus of the dispute: whether the “enterprise brings its own personnel” mode has commercial reasonableness and civil legitimacy

In practice, tax authorities and judicial authorities deny that the main reason for the arrangement of “enterprise-owned personnel” mode is that they believe that the platform enterprise intervenes in the established labor relationship for the purpose of issuing invoices, which lacks commercial reasonableness, and that the formation of the “three-party” business relationship has no legal basis. There is no legal basis for the formation of a “three-party” business relationship. However, this article believes that the above view is inconsistent with the business practice, contrary to the basic principles of civil law and tax law, and cannot be the reason for determining that the invoices issued under the mode of “enterprises with their own employees” are false invoicing. Specifically analyzed as follows:

(Ⅰ) The model of “enterprises with their own employees” is commercially reasonable.

According to the different sources of flexible employment personnel or drivers, the employment mode of platform enterprises can be divided into “platform organization personnel” mode and “enterprise-owned personnel” mode. In the “platform-organized personnel” model, the core function of the platform enterprise is to release demand information and match or screen the supply, and some platform enterprises also undertake auxiliary functions such as contract signing, fund settlement and tax payment. In the mode of “enterprises bringing their own personnel”, labor-using units and labor providers establish contact and reach cooperation on their own, and platform enterprises do not play the function of matching supply and demand. Some tax authorities and judicial authorities believe that the core function and advantage of the platform enterprise is to match supply and demand, and the supply and demand in the “enterprise-owned personnel” mode is already matched, so there is no need for the platform enterprise to intervene in the labor relationship, and there is no reasonable explanation other than cost reduction in violation of the law, and thus lacks commercial reasonableness.

However, the above point of view ignores the fact that platforms will inevitably generate new business values other than demand matching in the course of long-term development. In addition to the subjective willingness of enterprises to prefer to continue business with natural persons who have cooperated with them for a long period of time, the platform economy has developed so far, and platform enterprises have advantages that are difficult to be replaced by the direct labor model in terms of assumption of responsibility, business retention, tax compliance, and so on.

First, the inclusion of platform enterprises reduces labor risks. Under the direct labor mode, since natural persons are easy to lose contact with each other and their economic conditions are not rich, it is often difficult for laborers to recover all the losses when pursuing the contractual breach and tort liability of labor providers. Platform enterprises, as stable business entities, have higher solvency, and after the platform enterprises join the employment relationship, the employers can seek compensation from the platform enterprises for the damages caused by the labor providers to the employers, and the solvency rate is greatly increased.

Secondly, platform enterprises can solve the pain point of business trace. Some enterprises lack the awareness of compliance and do not pay attention to business traces, which makes it difficult to prove the real occurrence of expenditures and face the risk of false billing when being audited. In order to prove the business substance of invoicing, compliant platform enterprises can generally use digital tools to leave traces for the employment business, such as recording the service time and service content of flexible workers and drivers, real-time location of drivers, backing up data such as pound slips and GPS tracks, so as to prove that the three streams are one and the same.

Finally, the inclusion of platform enterprises helps tax compliance. Platform enterprises issue special VAT invoices to laborers in their own name to meet the tax needs of enterprises to obtain inputs and offset costs, reducing the incidence of white entry, and also assisting freelancers in completing personal tax declarations, ensuring tax compliance and preventing the spillover of personal tax risks.

(Ⅱ) Civil legitimacy of the “enterprise-owned personnel” model

Some tax authorities and judicial authorities believe that the platform enterprise's participation in the established employment relationship lacks legal legitimacy, and therefore deny the employment arrangement. However, the tax law, as a secondary adjustment law, is dependent on the underlying civil and commercial legal relationship. In other words, if the underlying civil and commercial legal relationship is legal, it is not appropriate to evaluate the illegality of the behavior from the level of the tax law, or to directly adjust the economic foundation through the underlying civil and commercial legal relationship.

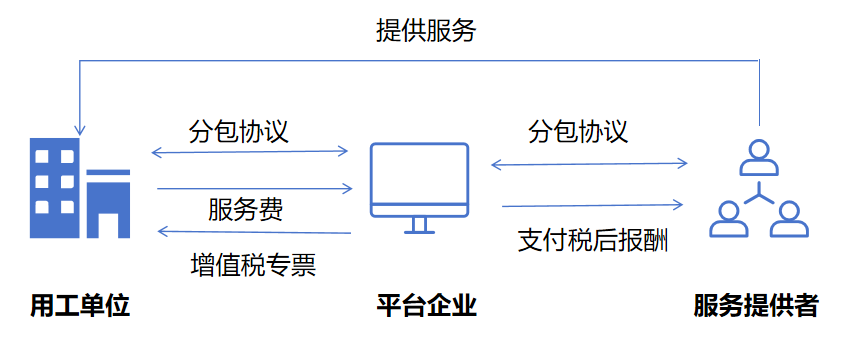

As shown in the above figure, the subcontracting agreement signed by the employing unit and the platform enterprise, the platform enterprise and the service provider is essentially a contract of entrustment or contract of contract of contract, which is protected by civil law, i.e., the platform enterprise joins the employing relationship with the basis of legitimacy of the civil law, and the personnel whether it is an enterprise organization or a platform organization doesn't affect the essence of the tripartite legal relationship. Moreover, as mentioned above, the platform enterprise's participation is commercially reasonable and does not satisfy the prerequisite of applying the principle of substantive taxation to the substantive adjustment of the civil legal relationship, and the legal arrangement of the platform enterprise's participation in the employment relationship should not be denied.

Ⅲ. Legal analysis: “enterprises with their own personnel” model does not meet the composition of false invoicing

(Ⅰ) The platform is based on a reasonable and legal business relationship, and the services provided are real.

In the case introduced, the enterprises involved in the case have truly employed riders and drivers to provide labor services, and the business can be proved through relevant order records, pound signs, driving records and other evidence. Despite the change in the mode of employment, the “enterprise with personnel” type of transaction does not change the nature of the taxable behavior, that is, as long as the three parties involved in the business to reach a civil level of agreement on the meaning of the employment of riders, drivers, whether affiliation with the platform to carry out the business, or take the business subcontracting, subcontracting way to carry out the business, should be treated as a platform to provide labor services. The labor service shall be regarded as provided by the platform. The platform enterprise provides real taxable services to the labor unit, and it is not improper for the platform enterprise to invoice accordingly.

(Ⅱ) There is no return of funds, and the payment of funds is real.

Some tax authorities and judicial authorities believe that any fund transfer to a private personal account provided by a downstream invoiced enterprise constitutes a reflux, therefore, even if the funds ultimately flow to the real service provider, but the person has a prior association with the invoiced enterprise, and the collection account is also provided by the recipient, it is considered that there is a reflux of funds.

This paper argues that this understanding is wrong and also disconnected from practice. Generally speaking, the flow of funds in the category of false invoicing is “invoiced party - invoicing party - invoiced party”. Although for the purpose of avoiding tax audits, multiple accounts of other enterprises or individuals may be inserted to go through the accounts, resulting in a complex and indistinguishable return chain, these accounts usually have one characteristic, i.e., they are under the actual control of the recipient enterprise or the invoicing enterprise, and the funds will ultimately flow to the public accounts of the recipient or the private accounts of the person in actual control. However, as in the case of the introduction of the case, although the account is provided by the invoiced enterprise, the invoiced unit is based on the account information provided for the purpose of providing the identity information of the flexibly employed person or the driver and the payroll list, and these accounts are not under the control of the invoiced enterprise, and the funds belong to the lawful remuneration of the real service provider, which has nothing to do with the invoiced enterprise, and therefore do not belong to the flow of funds back.

(Ⅲ) The invoices are consistent with the actual business operations and do not constitute false invoicing

Article 29 of the Implementing Rules for Invoice Management Measures divides false invoicing into “false invoicing without goods” and “false invoicing with goods” which is inconsistent with the actual business. In the “enterprise with personnel” type of transaction, there are real services, and the invoices issued by the platform faithfully reflect the real business, funds, invoices, services, “three streams of consistency”, does not comply with the definition of false invoicing in the administrative law, and the relevant invoices shall not be recognized as False invoicing.

(IV) Not disturbing the order of invoice management and not causing loss of tax

The invoices issued under the mode of “enterprises with their own personnel” faithfully reflect the real business, and both the invoicing by the platform enterprises and the offsetting by the invoiced enterprises are in compliance with the provisions of the law, which belongs to the link of free market transactions, and will not cause any disturbance to the national economic order, and have not disturbed the order of invoice management of the state. At the same time, since the invoiced enterprise has paid the full tax-inclusive price for the real transaction, it has the substantive right of deduction, and has not abused the right of deduction to cause the loss of national tax, which is not socially harmful.

IV. Suggestions: Strengthen business compliance management and do a good job of preventing beforehand and responding afterwards

(I) Platform enterprises should do a good job of prior compliance

Internet platform enterprises are prone to be involved in false driving cases, so it is all the more necessary to strengthen the construction of tax compliance. Specifically, in order to prevent the tax authorities and public security authorities from thinking that the labor services provided by flexibly employed persons and the transportation services provided by drivers have nothing to do with the platform enterprises, they should enter into a lawful agreement on the tripartite legal relationship before carrying out the business, and in particular, they should let the individuals who have actually provided the labor services or the services to make a clear expression of their intention, indicating that they are willing to provide the services to foreign countries in the name of the platform, and that they are affiliated to the platform to carry out the business or undertake the business assigned by the platform. or undertake the business assigned by the platform.

(Ⅱ) Actively responding to audits and criminal proceedings

For platform enterprises that have entered into audit or criminal proceedings, they should hire professionals to carry out communication or defense work from the perspective of the business model and its reasonableness. In recent years, more and more cases tend to deny the legitimacy and reasonableness of the business model of “enterprises with their own personnel”, and the risk and probability of constituting a crime for platform enterprises have increased, so they should proactively carry out the defense work by providing evidence and similar cases to strive for the optimal result.