The Relationship and Boundary Between the Crime of Falsely Issuing Special VAT Invoices, the Crime of Tax Evasion, and the Crime of Falsely Issuing Ordinary Invoices

Editor's Note: Two years have passed since the release of the Interpretation of the Supreme People's Court and the Supreme People's Procuratoracy on Several Issues Concerning the Application of Law in Handling Criminal Cases of Endangering Tax Collection and Administration (Fa Shi [2024] No. 4). During these two years, the Supreme People's Court has updated the National Unified Training Textbook for Judges, published typical cases on punishing crimes endangering tax collection and administration, issued a Reply to suggestions from People's Congress deputies regarding clarifying the nature of the act of "falsely crediting input tax" with falsely issued special VAT invoices, and judges from the Fourth Criminal Division have written the Understanding and Application of the new judicial interpretation. Judicial authorities nationwide, during investigation, prosecution, and trial stages, have fully implemented the spirit of the new judicial interpretation, shifting the conviction standards for crimes endangering tax collection and administration. Notably, they have fully clarified the boundary between the crime of falsely issuing special VAT invoices and the crime of tax evasion, forming an intertwined system of top-level legislative design, academic theory, and judicial practice for distinguishing criminality from non-criminality and one crime from another. This has played a significant role in safeguarding the application of the principle of suiting punishment to crime and protecting the development of private enterprises. The author attempts to summarize the relationship and boundary between the crime of falsely issuing special VAT invoices, the crime of tax evasion, and the crime of falsely issuing ordinary invoices for readers' reference.

I. The Crime of Falsely Issuing Special VAT Invoices and the Crime of Tax Evasion

Article 10 of Fa Shi [2024] No. 4 provides the judicial interpretation for the crime of falsely issuing special VAT invoices. Article 10 is divided into two paragraphs. The first paragraph specifies five types of specific acts constituting falsely issuing special VAT invoices. The second paragraph stipulates the circumstances for excluding liability for this crime, clarifying that "acts aimed at artificially inflating performance, financing, loans, etc., without the purpose of defrauding or crediting taxes, and which do not result in tax losses due to crediting, shall not be convicted under this crime; if they constitute other crimes, criminal liability shall be pursued according to law under those other crimes." Combining these two paragraphs reveals that committing the acts specified in the first paragraph does not automatically lead to conviction for the crime of falsely issuing special VAT invoices. Further investigation is needed into whether the party had the purpose of defrauding or crediting taxes and whether tax losses resulted from the crediting. It must be emphasized that causing a reduction in VAT payable through crediting based on falsely issued invoices might be considered a VAT loss from a tax perspective. However, this tax loss is not necessarily caused by the purpose of "defrauding or crediting" and does not necessarily constitute "tax loss due to fraud." Conviction for the crime of falsely issuing invoices requires proving the party's "fraudulent" intent.

According to Article 1 of Fa Shi [2024] No. 4, "Where a taxpayer makes a false tax declaration and falls under any of the following circumstances, it shall be deemed a 'deceptive or concealing means' as stipulated in Paragraph 1, Article 201 of the Criminal Law: ... (3) Falsely listing expenses, falsely crediting input tax, or falsely reporting special additional deductions." Including "falsely crediting input tax" as a criminal act under the crime of tax evasion indicates that using falsely issued special VAT invoices for crediting can constitute the crime of tax evasion. Combined with the exclusion clause for the crime of falsely issuing invoices, this shows that crediting based on falsely issued invoices could be aimed at "falsely crediting" (evading taxes) or "defrauding by crediting" (fraudulently obtaining state funds). To accurately convict, the boundary between "falsely crediting" and "defrauding by crediting" must be clarified.

Why distinguish between defrauding by crediting and falsely crediting? What is the fundamental difference in their social harm? The Understanding and Application points out that defrauding taxes by crediting "is essentially an act of defrauding state property with the purpose of illegal possession; imposing severe punishment conforms to the principle of suiting punishment to crime." The Reply further explains, "The crime of tax evasion is an act committed by a perpetrator based on evading tax obligations. Its harm lies in the loss of taxes that should have been collected due to non-payment. The crime of falsely issuing special VAT invoices involves the perpetrator exploiting the crediting function of special VAT invoices to issue false invoices and defraud state taxes. It is essentially an act of actively possessing state property through deceptive means, i.e., a fraud crime. Therefore, its harm is more severe than tax evasion, which also aligns with the Criminal Law's statutory penalty settings for the two crimes." Thus, defrauding by crediting emphasizes the purpose of illegal possession, defrauding state tax property, causing a loss of vested state interests (i.e., loss due to fraud), and is fraud in nature. Falsely crediting emphasizes evading taxes, underpaying taxes due, causing a shortfall in taxes that should have been collected, and is essentially a crime of evading tax debts. Consequently, the former is a felony subject to a maximum penalty of life imprisonment, while the latter is a misdemeanor subject to a maximum penalty of seven years' imprisonment.

So, what constitutes falsely crediting versus defrauding by crediting? How to distinguish whether a VAT loss is caused by falsely crediting or fraud? The Understanding and Application proposes an objective standard: whether the crediting through falsely issued invoices exceeds the scope of the tax obligation. "If a taxpayer, within the scope of their tax obligation, reduces tax payable by falsely increasing input tax for crediting, even if using falsely issued invoices for crediting, their subjective intent is still to not pay or underpay taxes. According to the principle of unifying subjective and objective elements, it should be convicted as the crime of tax evasion. This is the consideration behind Article 1, Paragraph 1, Item 3 of the Interpretation including 'falsely crediting input tax' as one of the 'deceptive or concealing means' for tax evasion." "If a taxpayer, exceeding the scope of their tax obligation, credits taxes by using falsely issued invoices, thereby not only evading tax obligations but also defrauding state taxes, then the part within the tax obligation scope constitutes the crime of tax evasion, and the exceeding part constitutes the crime of falsely issuing special VAT invoices. This is a concurrence of crimes where one act touches upon two charges and should be handled by choosing the heavier punishment."

For VAT, the scope of tax obligation is the output tax arising from actual sales, minus the input tax confirmed by invoices obtained from actual purchases. If a taxpayer falsely increases input tax by using falsely issued invoices and credits it within the scope of their tax obligation, their subjective purpose is not paying or underpaying taxes; this act constitutes tax evasion through falsely crediting input tax. If a taxpayer falsely increases input tax by using falsely issued invoices and credits it exceeding the scope of their tax obligation, according to current VAT regulations, the portion of input tax exceeding output tax can be applied for refund as excess input tax credit (留抵退税). The result is defrauding already collected taxes from the state treasury, infringing upon vested state tax interests, and possessing a fraudulent nature. The subjective purpose here is defrauding VAT by crediting; this act constitutes the crime of falsely issuing special VAT invoices.

II. The Crime of Falsely Issuing Special VAT Invoices and the Crime of Falsely Issuing Ordinary Invoices

According to Article 205a of the Criminal Law, "Whoever falsely issues invoices other than those specified in Article 205 of this Law, if the circumstances are serious, shall be sentenced to fixed-term imprisonment of not more than two years, criminal detention or public surveillance, and shall also be fined." Interpreting this article literally, the criminal object should be invoices other than special VAT invoices and other invoices usable for crediting taxes or defrauding export tax refunds, such as ordinary VAT invoices. It does not regulate the act of falsely issuing special VAT invoices. However, interpreting it teleologically yields a different conclusion. Criminal law protects legal interests. The boundary between crime and non-crime, and between one crime and another, lies in the presence or absence, and the type, of infringement upon legal interests. Correctly understanding criminal law hinges on correctly understanding the legal interests protected behind its provisions. Due to limitations in legislative technique, the wording of criminal law provisions cannot cover all aspects. Therefore, understanding criminal law solely through literal interpretation can lead to expansion or restriction. Only by understanding it based on the infringement of legal interests can one correctly distinguish between crimes.

From the perspective of legal interest infringement, special VAT invoices and ordinary invoices are not two completely separate things; they are in an inclusive relationship. Special invoices possess all functions of ordinary invoices, with the added function of tax crediting. The core difference between ordinary and special invoices lies primarily in this tax crediting function. Since two crimes are established for two objects that share an inclusive relationship, there must necessarily be a concurrence of legal provisions between them. In short, the difference between the crime of falsely issuing special VAT invoices and the crime of falsely issuing ordinary invoices does not lie in whether the formal object is a special or ordinary invoice, but fundamentally in which specific function of the invoice has been abused. In fact, the crime of falsely issuing special VAT invoices can be completely encompassed by the crime of falsely issuing ordinary invoices; it is a special case of the latter. The crime of falsely issuing special VAT invoices protects the tax crediting function of invoices and the VAT legal interest. The crime of falsely issuing ordinary invoices protects the collection and management function of invoices and the invoice management order. Falsely issuing special VAT invoices necessarily infringes upon the invoice management order but does not necessarily involve abusing the crediting function to cause fraudulent VAT losses. If a special VAT invoice is falsely issued without abusing the crediting function to cause such a loss, the result is no different from falsely issuing an ordinary invoice. In such a case, the legal interest protected by the crime of falsely issuing special VAT invoices is not implicated. The consequences of underpaying VAT or corporate income tax fall under the legal interest protected by the crime of tax evasion and should be evaluated by that crime. The consequence of disrupting the invoice management order falls under the legal interest protected by the crime of falsely issuing ordinary invoices and should be evaluated by that crime.

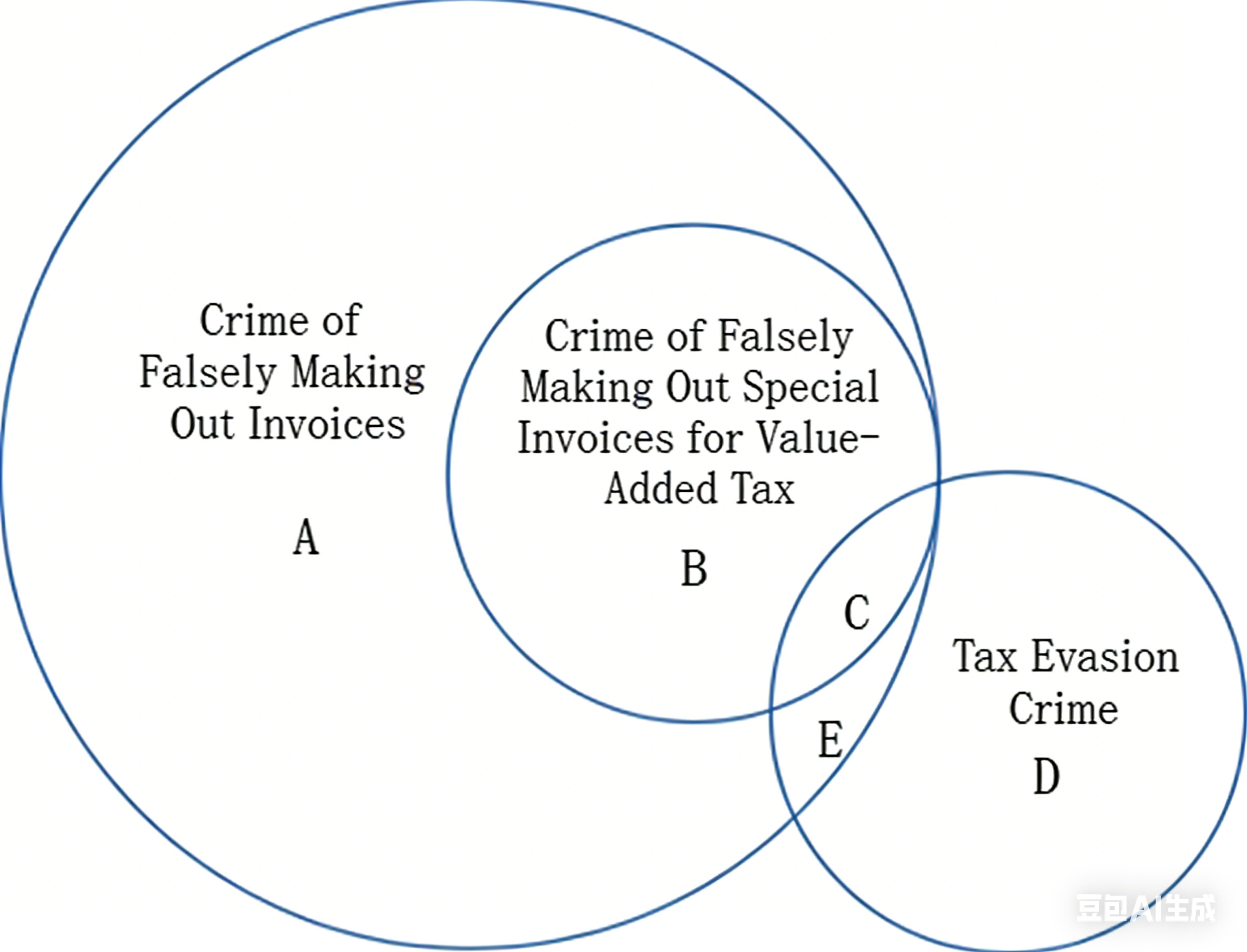

III. Illustrating the Relationship and Boundary of Three Types of Crimes Endangering Tax Collection with Examples

Combining the infringement of legal interests, the author believes the boundary between the three types of crimes should be as follows:

(Ⅰ)Area A:

Disrupts the invoice management order, but does not defraud VAT nor cause any reduction in tax obligations for any tax type. Constitutes only the crime of falsely issuing ordinary invoices.

Example: A company incurs expenses without invoices. According to Article 14 of the Measures for the Administration of Pre-tax Deduction Vouchers for Corporate Income Tax (SAT Announcement No. 28, 2018), it could use internal vouchers for pre-tax deduction, but this requires submitting numerous internal vouchers, a cumbersome process. For convenience, the company obtains falsely issued ordinary VAT invoices from a third party for expensing. From a tax perspective, the company's incurred expenses are deductible. Whether using internal vouchers or invoices for pre-tax deduction, the result is the same. Therefore, obtaining falsely issued invoices for expensing does not reduce the corporate income tax obligation. Since ordinary invoices lack the crediting function, it cannot reduce the VAT obligation or defraud VAT. However, obtaining falsely issued invoices infringes upon the invoice management order. If the amount reaches the threshold for criminalization, it constitutes the crime of falsely issuing ordinary invoices.

(Ⅱ) Area B:

Disrupts the invoice management order, and defrauds VAT, but does not cause any reduction in tax obligations for any tax type. Constitutes a concurrence of legal provisions between the crime of falsely issuing special VAT invoices and the crime of falsely issuing ordinary invoices, and is convicted as the crime of falsely issuing special VAT invoices.

Example: A shell company obtains falsely issued special VAT invoices to apply for excess input tax credit refunds. The shell company itself has no sales activities and incurs no tax obligations, making it impossible to cause a reduction in tax obligations. Its act of obtaining falsely issued special VAT invoices both disrupts the invoice management order and achieves the purpose and result of defrauding VAT through applying for refunds. This constitutes a concurrence of legal provisions and is convicted under the felony.

(Ⅲ) Area C:

Disrupts the invoice management order, defrauds VAT, and causes a reduction in tax obligations for some tax types. Constitutes a concurrence of legal provisions between the crime of falsely issuing special VAT invoices and the crime of falsely issuing ordinary invoices, and simultaneously an imaginative joinder with the crime of tax evasion. It is convicted as the crime of falsely issuing special VAT invoices.

Example: An operating entity has a VAT obligation of 10 million yuan. It obtains falsely issued special VAT invoices to falsely increase input tax by 20 million yuan. It applies for a refund for the excess part (10 million yuan) and also uses the falsely issued invoices for cost expensing in its accounts. First, obtaining falsely issued special VAT invoices disrupts the invoice management order. Second, booking the invoices and using them for cost expensing reduces corporate income tax payable, which should be evaluated by the crime of tax evasion. Finally, falsely increasing input tax beyond the output tax and applying for a refund indicates that the purpose was not just to underpay VAT but to defraud VAT, and this result occurred. This act should be evaluated by the crime of falsely issuing special VAT invoices. Regarding the tax evasion and the crime of falsely issuing special VAT invoices, one act touches upon two charges (imaginative joinder), and the conviction follows the heavier punishment.

(Ⅳ)Area D:

Does not disrupt the invoice management order, does not defraud VAT, only causes a reduction in tax obligations for some tax types. Constitutes only the crime of tax evasion.

Example: This refers mainly to acts that evade tax obligations without using invoices. For instance, an operating entity conceals income from sales to underpay VAT, corporate income tax, etc. This is tax evasion through concealing income. If the amount and proportion meet the criminalization threshold and the conditions for exemption are not met after the administrative pre-procedure, it constitutes the crime of tax evasion.

(Ⅴ)Area E:

Disrupts the invoice management order, does not defraud VAT, but causes a reduction in tax obligations for some tax types. Constitutes an implicated offense between the crime of falsely issuing ordinary invoices and the crime of tax evasion. It is generally convicted as the crime of tax evasion, but in special circumstances, as the crime of falsely issuing ordinary invoices.

Example 1: A taxpayer obtains falsely issued ordinary VAT invoices for expensing costs (as discussed in Area A).

Example 2: A taxpayer obtains falsely issued special VAT invoices for expensing costs and crediting input tax, but does not exceed the scope of their VAT obligation (i.e., the credited input tax is within the payable amount).

Analysis: For Example 1, falsely listing expenses is an act of tax evasion. As corporate income tax mainly operates on an invoice-based deduction model, falsely listing expenses is often achieved by falsely issuing invoices. When a taxpayer obtains falsely issued invoices for expensing costs, the means act (falsely issuing invoices) achieves the purpose and result of falsely listing expenses (tax evasion). The means act constitutes the crime of falsely issuing ordinary invoices, while the purpose act constitutes the crime of tax evasion. These form an implicated offense and should generally be convicted under the purpose act's crime (tax evasion). If the purpose act is exempted from criminal liability through the administrative pre-procedure for tax evasion, then the means act may be prosecuted as the crime of falsely issuing ordinary invoices.

Analysis for Example 2: This involves both falsely listing expenses and falsely crediting input tax, both of which are acts constituting the crime of tax evasion. As long as the falsely credited input tax from the obtained special invoices does not exceed the scope of the tax obligation, it falls under falsely crediting input tax, not defrauding VAT. This can be handled by analogy with Example 1, constituting an implicated offense. It must be emphasized that since VAT payable is calculated as output tax minus input tax, as long as the taxpayer's final declared input tax is less than the output tax (i.e., does not exceed the scope of the tax obligation), the result—whether achieved by concealing sales to reduce output tax or by falsely issuing input invoices to increase input tax—is merely reducing the tax payable and the tax obligation. There is no substantive difference between the two. If different legal evaluations are applied solely because falsely crediting input tax involved falsely issued invoices, while concealing income did not, it would seriously violate the principle of suiting punishment to crime.

IV. Conclusion

The new judicial interpretation has made significant adjustments to the conviction logic for crimes endangering tax collection and administration, providing basic guidance for judicial practice. However, in practice, some judicial authorities still fail to accurately grasp the spirit of the new interpretation. They continue to convict under the crime of falsely issuing special VAT invoices for cases that clearly fall under its exclusion clause, severely infringing upon the rights of the parties involved. Some local judicial authorities might not be unable to understand the new interpretation's spirit but are unwilling to understand, refuse to learn, hold conservative views, and remain stagnant. They fail to base judgments on facts and the law. Instead, they prioritize factors unrelated to the law, such as political background, economic effects, or social impact, as primary considerations in handling criminal cases, deviating from the core essence of judicial work. Acting against the current, based on the absurd principle that a severe sentence is better than a light one, and a wrong sentence is better than politically incorrect positioning, they still convict in cases meeting the exclusion criteria, severely harming parties' rights and fundamentally violating the spirit of the rule of law.

In response, the author believes that a normalized case error correction mechanism still needs to be established within the court system. Provincial High People's Courts should conduct secondary reviews of judgments within their jurisdiction, paying particular attention to judgments rendered by basic courts where there is significant dispute between prosecution and defense. They may report to the Supreme People's Court, ensuring the concept of the rule of law is implemented through effective institutional mechanisms and that courts can proactively identify miscarriages of justice based on their authority. Furthermore, the author believes that when non-judicial authorities discover cases suspected of criminal offenses, they may refer them to judicial authorities and be informed of the outcome. However, any interference in the judicial system must be strictly prohibited, including but not limited to assigning various tasks unrelated to case handling, requiring case-handling authorities to report progress periodically, organizing meetings to discuss or guide case handling work. Judicial adjudication power must be exercised solely by judicial authorities. Any interference with the judiciary is an overstep of power boundaries and a trampling of the rule of law. Judicial personnel must fully recognize their duties, respect their work, respect the authority granted by the state, stay away from political currents, return to professional work, and allow the new judicial interpretation to operate smoothly without hindrance.