Significant Regulatory Proposals Solicit Public Opinion! Tax Lawyers Interpret the Provisions on Tax Information Reporting for Internet Platform Enterprises

Significant Regulatory Proposals Solicit Public Opinion! Tax Lawyers Interpret the Provisions on Tax Information Reporting for Internet Platform Enterprises

Editor's note: From December 20, 2024 to January 19, 2025, the State Administration of Taxation issued the “Provisions on the Submission of Tax-related Information of Internet Platform Enterprises (Draft for Comments)”. (hereinafter referred to as the “Provisions”) to solicit opinions from the public. The draft of the Provisions was jointly drafted by the State Administration of Taxation and the State Administration for Market Regulation, aiming to further regulate the information submitted by Internet platform enterprises and promote the standardized, healthy and sustainable development of the platform economy. In view of this, we have interpreted the Provisions and put forward a number of suggestions for amendments based on the perennial observation and summary of the operation and development of Internet platforms.

I. The main contents of the “Provisions on the Submission of Tax-related Information of Internet Platform Enterprises”.

In recent years, with the rapid development of Internet technology, the development scale of China's platform economy has continued to expand. As platform enterprises rely on Internet technology to provide places and channels for many operators and practitioners, have a large number of users, and form a huge amount of data and information, which puts forward higher requirements for tax supervision and tax governance capabilities, some e-commerce enterprises and network anchors do not fulfill their tax obligations or evade taxes. To this end, the E-Commerce Law passed in 2018 clearly stipulates the tax-related information reporting obligations and legal liabilities of e-commerce platforms. Since then, the CPC Central Committee and the State Council have repeatedly issued important instructions and opinions on the supervision of internet platform enterprises; At the same time, since 2022, the tax authorities of five provinces and cities, including Tianjin, Jiangxi, Hubei, Hunan, and Guangdong, have carried out a pilot project for Internet platform enterprises such as online sales and webcasts to submit tax-related information on a quarterly basis. On this basis, the State Administration of Taxation and the State Administration for Market Regulation have launched the draft of the “Provisions” for comments, which mainly covers eight aspects:

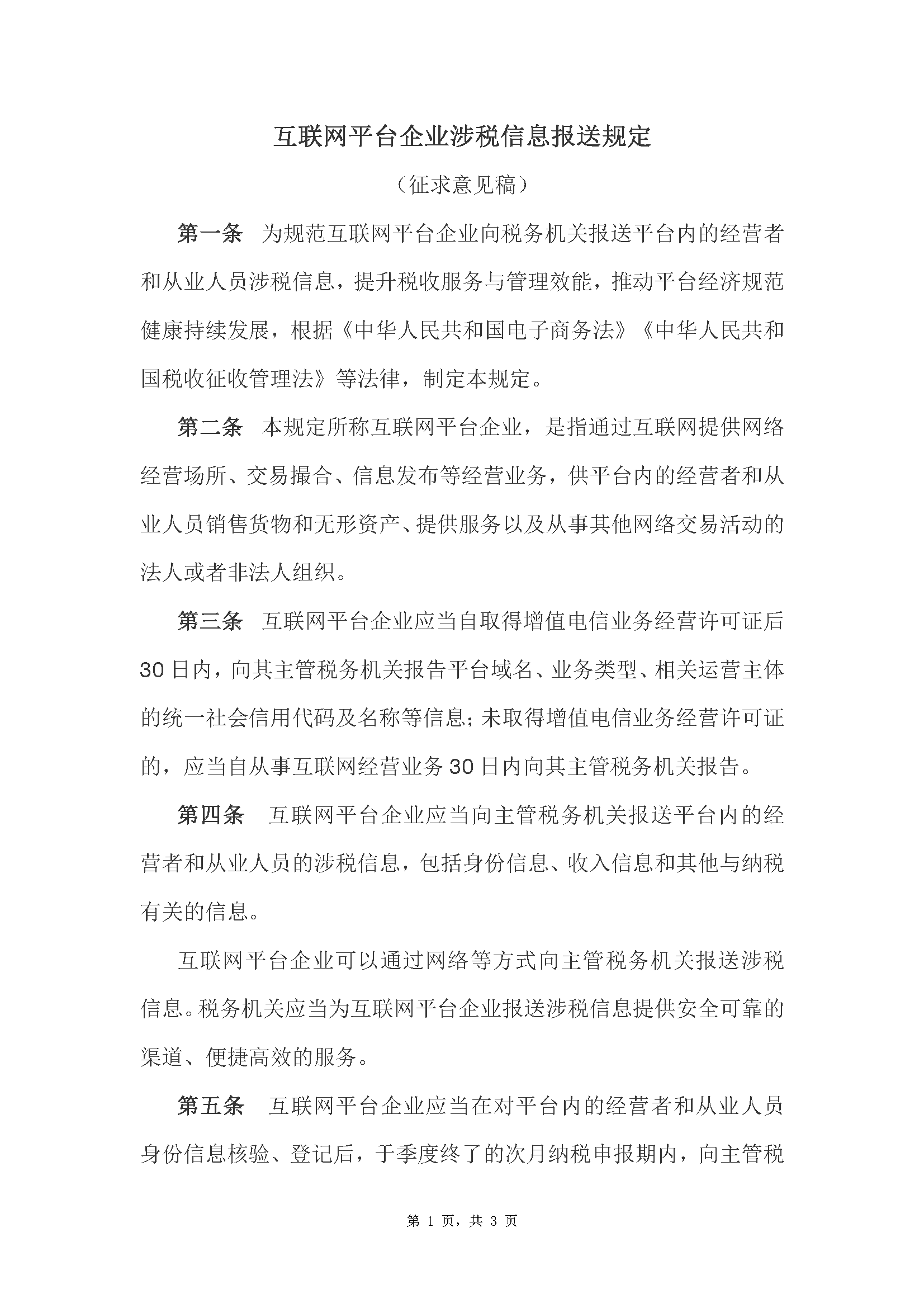

(I) The subject of the report

Article 2 of the Provisions stipulates that an internet platform enterprise “refers to a legal person or unincorporated organization that provides online business premises, transaction matchmaking, information release and other business operations through the Internet for the operators and employees on the platform to sell goods and intangible assets, provide services and engage in other online trading activities.” Accordingly, Internet platform enterprises have the following characteristics:

First of all, the business is to “provide network business premises, transaction matching, information release, etc.”; secondly, the purpose of the business is for the employees of the operators on the platform to sell goods and intangible assets, provide services, and engage in other online trading activities; Third, the business is characterized by relying on the Internet; Fourth, business entities include legal persons and unincorporated organizations.

(II) Platform enterprises' reporting obligations

According to Article 3 of the Provisions, an internet platform enterprise shall report to its in-charge tax authority within 30 days after obtaining a value-added telecommunications business license; Those who have not obtained a value-added telecommunications business license shall report to the in-charge taxation authorities within 30 days of engaging in Internet business business. That is, internet platform enterprises should first report their own information to the tax authorities and be included in the scope of management of the in-charge tax authorities. The content of the report is: information such as the domain name of the platform, the type of business, and the unified social credit code and name of the relevant operating entity.

This provision is the proper meaning of optimizing tax supervision and strengthening the performance of reporting obligations by platforms. However, there are the following problems in this article: first, whether the information of a platform that has obtained a value-added telecommunications business license can be transmitted synchronously from the Ministry of Industry and Information Technology, so as to strengthen information management and reduce the reporting obligations of the platform; Second, for enterprises that do not need to obtain, or have not yet obtained, value-added telecommunications business licenses, the scope of their “Internet business operations” is unclear, and it is unclear whether it overlaps with Article 2 of the Provisions; Third, if a platform enterprise fails to fulfill its reporting obligations, it has no corresponding legal liability.

(III) The obligation of platform enterprises to report tax-related information of business operators and employees

Articles 5 to 7 of the Provisions refine the tax-related information reporting obligations of platform enterprises, which are mainly divided into three parts:

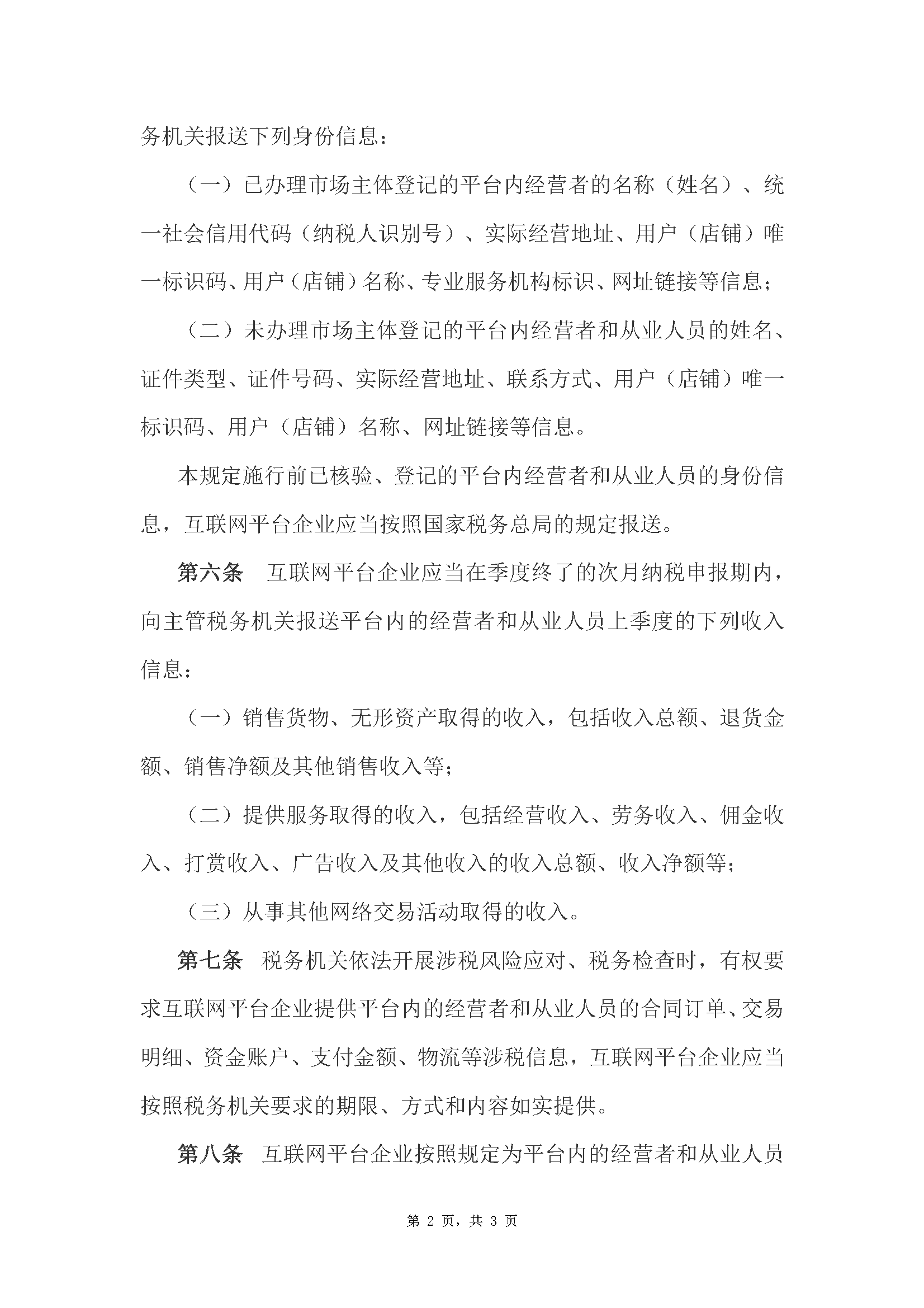

1. Identity information of business operators and employees

Internet platform enterprises shall submit different information based on whether the business operators and employees are registered as market entities. If a market entity has already been registered, such as an individually-owned business, sole proprietorship, company, partnership, etc., the name (name), unified social credit code (taxpayer identification number), actual business address, unique identification code of the user (store), name of the user (store), logo of the professional service organization, website link and other information shall be submitted.

If the market entity has not been registered, that is, the identity is a natural person, the name, certificate type, certificate number, actual business address, contact information, user (store) unique identification code, user (store) name, website link and other information of the operator and employee shall be submitted.

Submission time: Quarterly filing, the tax return period of the next month at the end of each quarter, that is, the tax return period of the 1st, 4th, 7th and 10th months.

2. Income information of business operators and employees

Internet platform enterprises shall report information on the income of the operators and employees on the platform in the previous quarter, including the income obtained from the sale of goods and intangible assets; income from the provision of services; Income derived from engaging in other online trading activities.

Submission time: Quarterly filing, the tax return period of the next month at the end of each quarter, that is, the tax return period of the 1st, 4th, 7th and 10th months.

3. Tax-related information required by the tax authorities

In addition to the above-mentioned routine submission information, internet platform enterprises shall still provide further truthful information on “contract orders, transaction details, capital accounts, payment amounts, logistics and other tax-related information of operators and employees on the platform” that need to be obtained by the tax authorities in accordance with the law when carrying out tax-related risk response and tax inspections in accordance with the law.

This article is in line with Article 57 of the Law on the Administration of Tax Collection, which stipulates that “when the tax authorities conduct tax inspections in accordance with the law, they have the right to investigate with the relevant units and individuals the circumstances of taxpayers, withholding agents and other parties in relation to the payment of taxes or withholding and remitting, collecting and remitting taxes, and the relevant units and individuals have the obligation to truthfully provide relevant information and supporting materials to the tax authorities”, which in essence refines the inspection power of the tax authorities in the field of Internet platforms.

(IV) Circumstances of exemption from reporting

Article 8 of the “Provisions” stipulates that some tax-related information platform enterprises of business operators and employees may be exempted from reporting, which includes three types of situations:

1. The withholding and payment and agency declaration information will no longer be submitted

When an internet platform enterprise has handled tax-related matters such as withholding declaration and agency declaration for the operators and employees on the platform in accordance with the regulations, it has already filled in the tax-related information, and the tax authorities have already mastered such information and do not need to submit it again.

2. The data provided by other departments will not be submitted

Internet platform enterprises are also not required to repeatedly submit tax-related information on operators and employees on the platform shared by the departments of industry and information technology, human resources and social security, transportation, market regulation, and internet information with the tax authorities.

3. Information in specific industries and fields is exempt from reporting

Internet platform enterprises may not submit information on the income of employees engaged in convenient labor activities such as distribution, transportation, and housekeeping.

(V) Service measures of the tax authorities

Article 9 of the Provisions clearly lists the types and contents of services provided by the tax authorities for the reporting entity, covering multiple fields such as information, technology and consulting, aiming to dredge the obstacles to the submission of tax-related information subjectively and objectively.

(VI) Information retention and confidentiality obligations

Article 10 of the Provisions stipulates that internet platform enterprises shall have the obligation to standardize the preservation and confidentiality of the tax-related information of the operators and employees on the platform.

(VII) Obligation to ensure the authenticity, accuracy and completeness of information

Article 11 of the Provisions stipulates that internet platform enterprises shall be responsible for the authenticity, accuracy and completeness of the tax-related information submitted. The original intention of this provision is to ensure that internet platform enterprises truthfully provide the information they obtain to the tax authorities, and to prevent internet platform enterprises from using false information to provide information on platform operators and employees without collecting and providing information as required, or jointly providing false information with platform operators and practitioners to help others evade taxes.

However, the disadvantage of this article lies in the fact that it does not explicitly require that platform enterprises be responsible for the information they obtain and monitor on the operators and employees of the platform. If there are operators or practitioners on the platform who deceive the platform by means such as “swiping orders”, resulting in the information collected by the platform being inaccurate, the platform shall not be responsible for such false data.

(VIII) Legal liability

Article 12 stipulates that if the platform fails to submit tax-related information in accordance with these provisions, it shall bear legal liabilities such as ordering corrections within a time limit, imposing fines or even ordering it to suspend business for rectification. The amount of the fine is: if the tax authorities order the correction within a time limit but refuses to make corrections, a fine of not less than 20,000 yuan but not more than 100,000 yuan shall be imposed; where the circumstances are serious, a fine of between 100,000 and 500,000 RMB is to be given. This article is linked to Article 80 (2) of the E-Commerce Law. However, it should be noted that the E-Commerce Law only regulates e-commerce platforms, while the penalties established in the Provisions regulate all Internet platforms, which is substantially larger than that of the E-Commerce Law.

According to Article 11 of the Administrative Punishment Law, “administrative regulations may set administrative penalties other than restrictions on personal freedom. “Where the law has already made provisions on administrative punishment for illegal acts, and administrative regulations need to make specific provisions, they must be provided for within the scope of the acts, types, and extent of administrative punishments prescribed by law. “The law does not provide for administrative punishment for illegal acts, and administrative regulations may supplement the administrative punishment for the implementation of the law. Where it is proposed to supplement the establishment of administrative punishments, opinions shall be widely heard through means such as hearings and debate meetings, and a written explanation shall be made to the formulating organ. When administrative regulations are submitted for filing, the circumstances of supplemental administrative punishment shall be explained. “Specifically, the administrative penalties provided for in this article of the “Provisions”, in which the penalties involving e-commerce platforms belong to the specific implementation of the provisions of the “E-Commerce Law”, and those involving platforms other than e-commerce platforms belong to the supplementary establishment of the law without administrative law provisions, and the procedures for extensive hearing of opinions shall be performed.

II. Main highlights of the Provisions on the Submission of Tax-related Information by Internet Platform Enterprises

On the basis of the E-Commerce Law, the Provisions expand the scope of Internet platforms, refine the scope of information to be submitted, reduce the burden on platform enterprises to a certain extent, and clarify the legal responsibilities of platform enterprises. Specifically, there are 5 highlights:

(I) The scope of reporting entities has been expanded to cover platforms such as online livestreaming

Article 2 of the Provisions has expanded the scope of the Provisions compared with the provisions of the E-Commerce Law. Article 2 of the E-Commerce Law stipulates that: “The term “e-commerce” as used in this Law refers to the business activities of selling goods or providing services through the Internet and other information networks. “At the same time, it is stipulated that this law does not apply to financial products and services, and the use of information networks to provide services such as news information, audio and video programs, publishing, and cultural products.” However, the Provisions are not limited to the scope of e-commerce platforms, nor do they adopt the provisions of the E-Commerce Law that exclude financial, news, audio and video programs, publishing and cultural products, which means that many Internet platforms that provide news, audio and video, and cultural products, as well as the operators and practitioners on the platforms, will be included in the scope of management. It can be seen that the Provisions are not completely subordinate to the E-Commerce Law, but regulate all Internet platform enterprises, including e-commerce platforms.

The main impact of Article 2 of the Provisions is that it includes online live streaming platforms. In recent years, the online live broadcast industry has risen rapidly with the rapid development of Internet technology, the scale of users has continued to expand, and the market scale has continued to grow, especially during the epidemic, live broadcast e-commerce has become a major bright spot, driving the further development of the industry and giving birth to a group of high-income online live broadcast practitioners. Since the beginning of this year, the State Administration of Taxation has announced a number of typical cases of tax evasion by online live broadcast practitioners, demonstrating the country's determination to rectify the chaos of online live streaming and strengthen tax supervision.

(II) The scope of the information to be submitted is clarified and refined, and it is operable

Articles 5 to 7 of the Provisions refine the scope of information to be submitted by platform enterprises, including identity information and income information, with the following characteristics:

First, it mainly emphasizes the provision of total revenue information, mainly because platform enterprises usually provide payment systems, which can grasp the income information of operators and employees on the platform, or the net sales or income after deducting platform commissions or service fees, but cannot grasp the expenses and costs of operators and employees;

Second, it clarifies that the income obtained from the provision of services includes “business income, labor income, commission income, reward income, advertising income and other income”, covering all possible forms of income, and can prevent operators and employees from switching income forms to avoid reporting obligations;

Third, the quarterly submission of tax-related information is to take into account that some operators themselves are enterprises and have declared and paid taxes to the tax authorities, so the main role of submitting tax-related information is to compare the accuracy and authenticity of tax declarations, so there is no need to submit information on a monthly basis.

Compared with the broad and abstract provisions of the E-Commerce Law, the above-mentioned provisions are more feasible and conducive to implementation in practice.

(III) Avoid duplicate reporting of information, reducing the burden on the platform

Since Internet platform enterprises are oriented to a large number of unspecified operators and practitioners, they have an agglomeration effect. Moreover, the more leading platform enterprises, the greater the number of operators and employees who will settle on the platform, so the reporting obligation will inevitably bring a burden to the platform. To this end, it is important to clarify the scope of an exclusion from reporting. The scope of exemption from reporting determined by the “Provisions” can better reduce the burden on the platform.

For the first type of internet platform enterprises, which have already handled individual income tax withholding and payment for their employees, or filed for them on behalf of their employees, they may no longer submit relevant tax-related information, considering that most of the employees on many platforms, especially live streaming platforms and video platforms, are natural persons rather than enterprises. According to the Administrative Measures for the Withholding and Declaration of Individual Income Tax (for Trial Implementation) (Announcement No. 61 [2018] of the State Administration of Taxation), when a natural person obtains income from other tax purposes other than business income, the entity or individual that pays the income to the natural person shall perform the individual income tax withholding and payment obligation. Therefore, when the platform pays the wages and labor expenses of employees, it shall perform the withholding and payment obligations in accordance with the law, and the tax authorities have already mastered such information, so there is no need to submit it repeatedly. A similar approach is the case for the second category of other sectors that share revenue information.

(IV) Specific industries are exempt from reporting, with a focus on supervising high-income groups

In particular, the “Provisions” exclude employees of “convenient labor activities such as distribution, transportation, and housekeeping” from the scope of reporting obligations, and give them the right to be exempted from reporting. According to the interpretation of the State Administration of Taxation's “Drafting Instructions on the Provisions on the Submission of Tax-related Information for <Internet Platform Enterprises (Draft for Comments>)” of the State Administration of Taxation, it is taken into account that “employees in the platform with a comprehensive annual income of no more than 120,000 yuan basically do not need to pay individual income tax or only need to pay a small amount of tax after deducting expenses and special additional deductions such as children's education and supporting the elderly.” Because of this, the income information of food delivery workers, couriers, domestic workers, online car-hailing drivers, online freight drivers and other personnel may not be submitted in accordance with the requirements of the “Regulations”. That is, considering that the income of related industries is generally limited, most of them do not pay taxes or pay less taxes. Therefore, the main purpose of the promulgation of the “Provisions” is to supervise high-income e-commerce and online live broadcast operators and practitioners, and to maintain the principle of tax fairness.

(V) Emphasizing that the tax authorities should provide corresponding services to facilitate information reporting

With the development of Internet platforms such as e-commerce, online live broadcasting, social networking, video, and blogs, the leading platforms have absorbed a huge number of operators and practitioners. At the same time, due to the low threshold for carrying out business activities on the platform, many natural person consumers also have a tendency to become employees, further expanding the scope and group of platform enterprises' reporting obligations. Therefore, it is necessary for the tax authorities to provide corresponding information network technical services to ensure that platform enterprises can submit relevant data on a quarterly basis, otherwise many platforms may objectively not have the ability to collect and summarize relevant data.

III. Suggestions for revising the Provisions on the Reporting of Tax-related Information by Internet Platform Enterprises

Based on the above analysis, the following amendments are proposed to address some of the deficiencies of the Provisions:

(I) Limit the scope of internet platform enterprises and avoid excessive scope

Scope of amendment: Article 2 of the Provisions

Suggestion for amendment: A paragraph is added as the second paragraph: “These provisions do not apply to the use of information networks to provide services such as news information, articles, and broadcasting.” “

Reason for amendment: The scope of Internet platform enterprises in Article 2 of the Provisions is determined through two levels: the first level is that platform enterprises should have the ability to provide online business venues, transaction matchmaking, and information release, which is a requirement for the platform itself; The second level is that operators and practitioners on the platform should rely on the platform to carry out sales of goods and intangible assets, provide services and engage in other online trading activities, which is a requirement for operators and practitioners.

However, the above-mentioned regulations alone are too broad and easy to include the relevant services of a large number of Internet companies, such as article publishing, Q&A platforms, and audio podcast platforms. With the development of such platforms, the platform provides “rewarding” or paid services and sales functions for eligible accounts, so that such platforms are no longer free information publishing platforms in the past, but also become paid online trading activities, so that there is a possibility of being included in the scope of management. However, from the perspective of the market, text, news, Q&A, and audio podcasts alone are not enough to bring high income to employees, and their benefits are relatively limited, and cannot be compared with video platforms and live broadcast platforms, and the number of employees engaged in such article writing and audio podcast publishing is more than that of video and live broadcast personnel, resulting in excessive reporting obligations of platforms, which should be excluded with reference to the provisions of the E-Commerce Law.

(II) Limit the scope of “engaging in internet business operations”.

Scope of amendment: Article 3 of the Provisions

Suggestion for amendment: “Those who have not obtained a value-added telecommunications business license shall report to their competent tax authorities within 30 days of engaging in Internet business business.” “Amendment” is amended to read: “Those who have not obtained a value-added telecommunications business license shall report to the competent tax authorities within 30 days of engaging in the Internet platform business provided for in Article 2 of these Provisions.” “。

Reason for amendment: Article 3 of the Draft Provisions stipulates that even if an enterprise has not applied for a value-added telecommunications business license, but has already carried out relevant Internet business business, it shall report its own information to the tax authorities in a timely manner to facilitate the management of the tax authorities. However, the scope of Internet business is too broad, including not only Internet platform enterprises, but also other businesses that do not involve platforms, such as web browsing and information publishing. Therefore, all Internet operations should not be included in the reporting obligation and should be restricted.

(III) Coordination of issues where the platform is inconsistent with the location of business operators and practitioners

Scope of amendment: Article 9 of the Provisions

Suggestion for amendment: A new paragraph is added as the second paragraph: “The tax authorities shall establish an information sharing mechanism to pass on tax-related information to the competent tax authorities of business operators and practitioners.”

Reason for amendment: The Provisions require platform enterprises to submit all tax-related information to the competent tax authorities of platform enterprises, but the operators and employees on the platform are distributed throughout the country and are not subject to the jurisdiction of the competent tax authorities of platform enterprises, but are managed by their local tax authorities with jurisdiction. Therefore, it is necessary to establish a corresponding information sharing and transmission mechanism, otherwise even if relevant tax-related information is collected, it will not be able to play a corresponding role.

(IV) Increase the provision on the delimitation of the scope of exclusion according to the total annual income

Scope of amendment: Paragraph 1 of Article 8 of the Provisions

Suggestion for amendment: “The income information of employees engaged in convenient labor activities such as distribution, transportation, and housekeeping on the platform may not be submitted.” It is amended as: “The total annual income of the platform does not exceed 120,000 yuan, or the income information of employees engaged in convenient labor activities such as distribution, transportation, and housekeeping may not be submitted.” “

Reason for revision: The State Administration of Taxation's “Drafting Instructions on the Provisions on the Submission of Tax-related Information for <Internet Platform Enterprises (Draft for Comments>)” of the State Administration of Taxation proposes that the reason why industries such as distribution, transportation, and housekeeping are exempted is because their total annual income is generally lowMost practitioners do not pay taxes or pay little or no taxes. However, considering that the income of many employees on the platform is also low, such as the bottom live broadcast and video employees, whose number is huge but the income does not exceed 120,000 yuan, they should be exempted to further reduce the reporting obligation of the platform.

(V) Increase the liability exemption system for false information submitted due to the responsibility of business operators

Scope of amendment: Article 11 of the Provisions

Suggestion for amendment: A paragraph is added as the second paragraph: “If the tax-related information is false due to the responsibility of the operators and employees on the platform, the operators and employees shall bear legal responsibility.” “

Reason for amendment: From the perspective of the actual operation process, an internet platform enterprise can only be responsible for the tax-related information it monitors and collects, but cannot be responsible for the objective authenticity, reliability and accuracy of the tax-related information. If the platform cannot identify the platform due to the limited regulatory capacity due to the deception of the operators on the platform, such as bypassing the platform to collect money privately, or “swiping orders” to inflate revenue and costs, etc., the platform shall not be liable for such liability.

Attachment: Full text of the Provisions on the Submission of Tax-related Information by Internet Platform Enterprises (Draft for Comments).