CRS Financial Account Information Exchange accurately identifies untaxed income from overseas stock speculation, how to resolve tax-related risks?

Recently, many domestic individuals who opened financial accounts in Hong Kong to speculate on U.S. stocks have received SMS notifications from tax authorities around the world, suggesting that they have overseas income that has not been declared as taxable in accordance with the law and requesting them to self-examination and declaration of back taxes. How do China's tax authorities obtain information on the financial accounts opened by domestic individuals in Hong Kong or abroad, and how do they grasp the behavior and income from overseas stock investments? Does a domestic individual need to declare tax in China for the income from investment and wealth management in overseas securities market using financial accounts outside of Mainland China, what legal responsibility will he/she face if his/her income from overseas stock speculation is discovered by the tax authorities without tax declaration, and how to solve the tax-related risks? This article discusses and analyzes a specific case.

I. the actual case to share: the domestic individual speculation in U.S. stocks by the tax authorities require self-examination to make up taxes

In 2020, Zhang's friends through the securities investment gained considerable income, Zhang began to learn stock investment knowledge. 2021 early, Zhang through a Hong Kong brokerage firm APP opened a U.S. stock account for a number of U.S. stock short-term trading. The profit and loss situation of Zhang's U.S. stock speculation was an overall profit of 100,000 U.S. dollars in 2021, a loss of 200,000 U.S. dollars in 2022 due to the impact of the bear market, and an overall profit of 200,000 U.S. dollars in 2023,” Zhang said.

Recently, Zhang received a text message notification from the competent tax authority at his workplace, prompting him to conduct self-checks and pay back taxes on the foreign income he received. Zhang paid no attention to it. Recently, Zhang received another phone call from a staff member of the tax authority, who informed Zhang that he had conducted securities transactions through an overseas brokerage platform, and that Zhang had undeclared overseas income, and requested Zhang to pay the back taxes as soon as possible. Zhang believed that these gains were not sourced from within China and did not need to pay individual income tax. If he needs to pay, he should only pay individual income tax on the net income of 100,000 US dollars.

How did the tax authorities in Zhang's workplace find out that Zhang had obtained income from overseas stock investments? Is Zhang's argument valid?

II. How do tax authorities detect foreign income derived from foreign stock investments?

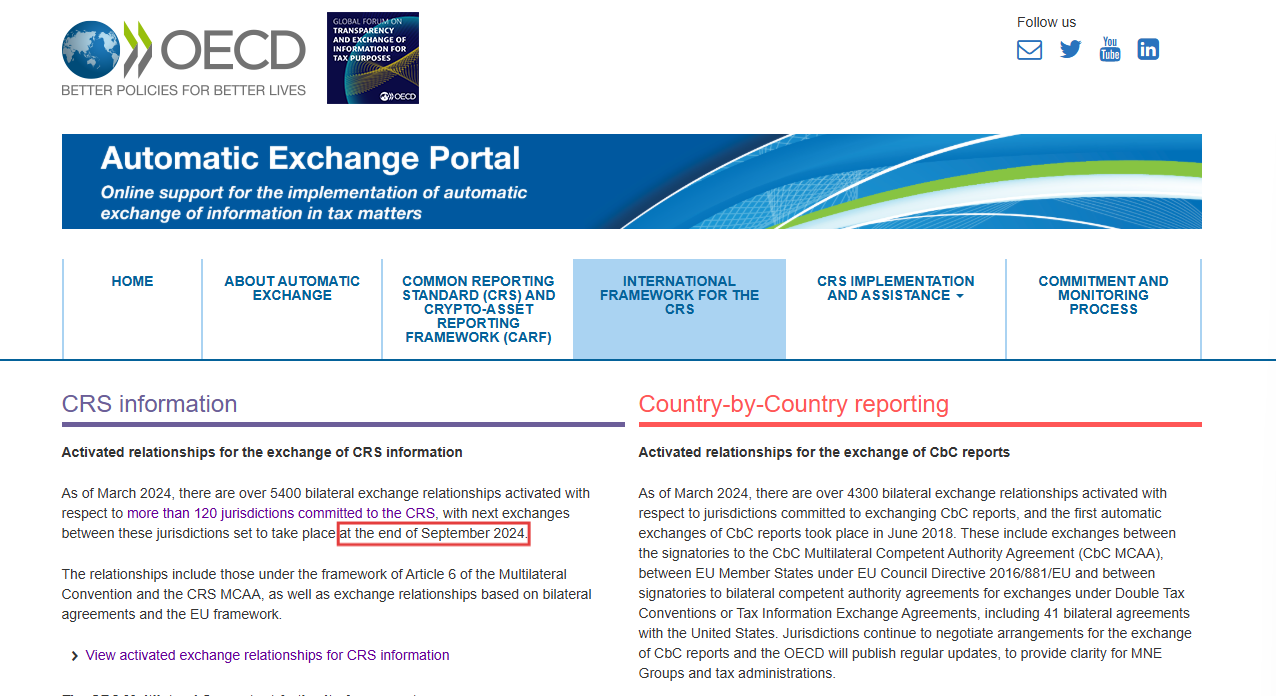

In order to strengthen cross-border tax cooperation, enhance tax transparency and combat cross-border tax evasion, the Organization for Economic Cooperation and Development in Asia and the Pacific (OECD) issued the Standard for Automatic Exchange of Tax-Related Information (AEOI) on Financial Accounts (AEOI) in 2014, which is used to guide the participating jurisdictions to exchange information on tax residents' financial accounts on a regular basis. This standard consists of two main parts: the Model Competent Authorities Agreement (MCAA), which mainly stipulates how the automatic exchange of tax-related information on financial accounts is to be carried out between tax authorities of various countries; and the Uniform Reporting Standard (CRS), which mainly stipulates that The second is the “Uniform Reporting Standard” (CRS), which mainly stipulates the relevant requirements and procedures for financial institutions to identify, collect and report information on foreign tax residents.

In September 2014, China committed to implement AEOI at the G20 meeting.In July 2015, China's National People's Congress ratified the Multilateral Convention on Mutual Assistance in Tax Administration, laying a multilateral legal foundation for the implementation of AEOI.In December, the State Administration of Taxation (SAT) signed the Multilateral Competent Authorities Inter-Authority Agreement for the Automatic Exchange of Tax-Related Information on Financial Accounts (AEOIFA), which provides the mechanism of cross-border exchange of information on financial accounts with a multilateral legal tool at the operational level. In May 2017, the State Administration of Taxation (SAT) issued the Administrative Measures for Due Diligence on Tax-Related Information on Non-Resident Financial Accounts, which clarified the due diligence behavior of financial institutions in China on tax-related information on non-resident financial accounts.In September 2018, the SAT exchanged information with tax authorities of other countries (regions) for the first time.

Hong Kong, as a global financial center, has committed to implementing AEOI and commencing the first exchange of information by the end of 2018.

Part 8A (Part 8A) of the Inland Revenue Ordinance (IRO) of Hong Kong serves as the basic legal framework for CRS in Hong Kong. In addition, Hong Kong has issued the Guidelines for Financial Institutions, and financial institutions in Hong Kong have fulfilled their due diligence obligations in accordance with the abovementioned provisions, and have identified, collected and reported tax-related information on financial accounts in accordance with the regulations.

Specifically in this case, Zhang used a Hong Kong brokerage firm's APP to speculate on stocks, and the brokerage firm should perform due diligence procedures in accordance with the CRS rules formulated by the OECD, and has the obligation to identify, collect and report the tax-related information of the financial account, including the collection of information on the account opened by Zhang, his name, country of residence for tax purposes, taxpayer identification number, address of his current address, his place of birth, date of birth, and the total amount of income received or credited to the account during the calendar year, and declare such tax-related information of Zhang to the Hong Kong tax authorities. The IRD will report the tax-related information of Zhang to the Hong Kong Inland Revenue Department (IRD). The Hong Kong Inland Revenue Department then exchanged the tax-related information with the State Administration of Taxation (SAT). The State Administration of Taxation then passes the tax-related information to the tax authorities in Zhang's place of work.

According to the official website of OECD, the latest CRS financial account tax-related information exchange has been completed in September 2024, according to which, I speculate that the relevant account information obtained by the tax authorities in Zhang's workplace is very likely to be exchanged in September 2024, and the exchange of account information belongs to the period from the year 2021 to the year 2023.

It is important to pay attention to the difference between bank accounts and non-bank accounts in terms of the nature of the use of funds in the account. The use of funds in bank accounts is more diversified, while the use of funds in non-bank accounts is more single and easier to be recognized by tax authorities. In this case, Zhang's financial account was used exclusively for foreign stock investment, which exposed him to greater tax risk. The single purpose of the funds determined that the tax authorities were able to accurately identify that Zhang's foreign income was derived from stock investment.

III. Should the income of domestic individuals from overseas stock investment be subject to individual income tax in China?

Article 1 of the Individual Income Tax Law stipulates that “Individuals who have a residence in China or who do not have a residence but have lived in China for a total of 183 days in a tax year are resident individuals. Individuals who are residents shall pay individual income tax on the income they derive from within and outside China in accordance with the provisions of this Law. Individuals who do not have a domicile and do not reside in China, or individuals who do not have a domicile and have resided in China for less than 183 days in a taxable year, are non-resident individuals. Non-resident individuals shall pay individual income tax on the income they derive from the territory of China in accordance with the provisions of this Law”. Article 10 stipulates that “In any of the following cases, the taxpayer shall make a tax declaration in accordance with the law: (4) Acquisition of overseas income”.

Accordingly, if a natural person is recognized as a resident individual, he/she has to bear unlimited tax obligations, and the taxable income he/she obtains, regardless of whether he/she obtains it from the territory of China or from outside of China, he/she has to pay individual income tax in China. If a natural person is determined to be a non-resident individual, he/she is subject to a limited tax obligation and is required to pay individual income tax to the tax authorities in China only in respect of his/her income derived from within the territory of China.

Specifically in this case, Zhang is a citizen of China, with nationality, household registration and residence in China, and constitutes a resident individual of China, who is subject to unlimited tax liability and is required to pay individual income tax on the income derived from overseas stock investment.

IV. How to calculate the amount of individual income tax payable on income from overseas stock investment?

Article 1 of the Announcement on Relevant Individual Income Tax Policies on Overseas Income (Announcement of the Ministry of Finance and the State Administration of Taxation No. 3 of 2020) stipulates that “the following income shall be income derived from sources outside of China: ...... (v) interest obtained from enterprises and other organizations outside of China, as well as from non-resident individuals, dividends and bonus income; ...... (vii) Income derived from the transfer of shares formed from investments in enterprises and other organizations outside China ......”. Article 3 of the Individual Income Tax Law stipulates that “the tax rate of individual income tax: (3) interest, dividend and bonus income ...... from property transfer shall be subject to a proportional tax rate of twenty percent”.

Accordingly, the income derived from Zhang's overseas stock investment consists of two parts: first, the dividend income derived during the period of holding the stock. The second is the capital gains from the transfer of stocks. The tax rate for both dividend income and property transfer income is 20%.

On the issue of how to pay individual income tax on dividend income derived from Zhang's overseas stock investment, the tax rules are clearer and basically there is no dispute. This article will not go into details here.

On the issue of how to pay individual income tax on capital gains from Zhang's overseas stock investment, there is no capital gains tax related to stock investment in China. Since there is no tax item related to capital gains in China, the tax item related to capital gains is “income from transfer of property”, therefore, the capital gains made by Zhang's overseas stock investment should be subject to individual income tax in accordance with the rule of “income from transfer of property”.

Article 6 of the Individual Income Tax Law stipulates that “Income from the transfer of property shall be taxable as the income from the transfer of property, less the original value of the property and reasonable expenses”. Article 17 of the Regulations for the Implementation of the Individual Income Tax Law provides that “Income from the transfer of property shall be taxed on the basis of the income from a single transfer of property, less the original value of the property and reasonable expenses”. It can be seen that the taxpayer should calculate the taxable income on the basis of one transfer of property.

The second paragraph of Article 12 of the Individual Income Tax Law provides that “taxpayers shall calculate the individual income tax on a monthly or per-transfer basis for the income derived from the transfer of ...... property”. Accordingly, income from property transfers should be declared on a monthly or timeshare basis.

In summary, the current tax law stipulates the calculation method and tax declaration rules for the income from property transfer, but it does not clarify whether the income and loss can be offset if stocks are bought and sold several times in a tax year.

In this regard, the State Administration of Taxation (SAT) has clearly pointed out in its reply to the reporter's question on “Notice on Clarifying the Caliber of Self-Tax Declaration for Income Above 120,000 Yuan Per Annum” (Guo Shui Han [2006] No. 1200) that the income from the transfer of stocks is taxed according to the income from each “times” under the current itemized tax system model, and that the different “times” of income are taxed according to the income from each “times” of the transfer of stocks. Under the current itemized tax system, the income between different “times” is not allowed to offset the profit and loss, that is to say, if there is any gain, it should be taxed, and if there is no gain, it will not be taxed.

Accordingly, the capital gains derived from Zhang's foreign stock investments are property transfer income and are subject to individual income tax based on the income derived from each stock transaction. Taking the year 2022 as an example, although Zhang has an overall loss of $100,000, if one of the stock transactions generates capital gains, he also needs to pay individual income tax at a separate rate of 20%.

In the author's opinion, whether the profit and loss of multiple transfers of the same type of property in a tax year can be offset is a legal gap, and the current tax law only provides for the method of calculating taxable income and the method of tax declaration, and does not explicitly allow or prohibit the offsetting of income and loss. In the author's opinion, whether gains and losses from multiple transfers of the same kind of property in a tax year can be offset is a legal gap, and the current tax law only provides for the calculation of taxable income and tax declaration methods, and does not explicitly allow or prohibit the offsetting of gains and losses. According to the principle of taxing according to capacity and the principle of proportionality, Zhang can still try to communicate with the tax authorities to seek a balance between the taxing rules and the fairness of taxation. Specifically:

The principle of tax according to ability requires that the amount of tax payable be determined according to the taxpayer's ability to pay tax or financial burden, with those who have strong ability to pay tax paying more, those who have weak ability to pay tax paying less, and those who do not have the ability to pay tax paying no tax. In this case, Zhang had losses in the process of overseas stock investment, and the requirement to pay individual income tax on the capital gains of each stock transaction obviously exceeded his tax capacity, which was inconsistent with the principle of tax according to ability.

The principle of proportionality requires the tax authority to choose the way that minimizes the damage to the relative's rights and interests when there are various ways to effectively achieve the administrative objectives. If the loss of Zhang's overseas stock investment is not taken into account, and he only made a gain of 100,000 US dollars, the tax authorities require him to pay individual income tax on the capital gain of each stock transaction, which is far beyond the necessary limit of the tax authorities to collect tax, and it substantially damages the property rights and interests of the taxpayers, and also fails to realize the taxing purpose of the individual income tax to regulate the distribution of income and to promote the social fairness.

V. How to solve the tax-related risks after receiving the risk reminder from the tax authority?

Domestic individuals should not be paralyzed after receiving a notice from the tax authority requesting them to check and pay tax. The fact that the tax authority obtains tax-related information on the overseas financial accounts of domestic individuals through CRS and issues a risk reminder does not mean that it has sufficient evidence that the domestic individuals have not declared tax on their overseas incomes. However, according to the “five-step working method” enforcement procedure of “prompting and reminding, supervising and rectifying, interviewing and warning, filing and auditing, and public exposure” of the tax authorities, if the domestic individual refuses to make up the tax payment, the tax authorities will, according to the law If the domestic individual refuses to make up the payment, the tax authorities will initiate the audit procedure according to the law, carry out a comprehensive investigation, and require the domestic individual to provide the corresponding evidence and materials. The tax authorities will fully grasp the evidence and materials of the domestic individual's undeclared tax payment for the overseas income and form a complete chain of evidence. In this case, according to the provisions of the Law on Administration of Tax Collection, if the tax authorities order the domestic resident individual to pay back tax on the undeclared foreign income, and the domestic resident individual still refuses to pay, this constitutes tax evasion of “refusing to declare after notification to declare”, and his/her tax risk is directly escalated, and in addition to paying back the tax and late fees, he/she will also be In addition to paying back taxes and late payment fees, the tax risk faced by the company will be directly escalated.

Based on this, the author suggests that domestic individuals should pay attention to the requirements of CRS tax compliance, and file tax returns on overseas income in accordance with the law and in a timely manner, so as to avoid unnecessary tax disputes. In case of tax disputes, resident individuals should respond prudently by actively communicating with tax authorities, making statements and defenses in accordance with the law, and seeking legal remedies and professional support from tax lawyers in a timely manner, in order to strive for a fair and reasonable payment of back taxes, and at the same time, they can refer to the “Approval Response from the State Administration of Taxation on the Issues of Undeducted Individual Income Tax to be Deducted by the Administrative Organs” (GuoShuiHuan [2004] No. 1199) At the same time, you can refer to the “Approval Reply of the State Administration of Taxation on the Issue of Individual Income Tax Not Withheld by Administrative Organs” (Guo Shui Han [2004] No. 1199), and strive for the non-payment of late payment fees. In addition, residents need to pay attention to the legitimacy of the source of funds from abroad, avoiding the implementation of illegal foreign exchange trading behaviors, such as buying and selling foreign exchange or trading foreign exchange in disguise, in order to prevent constituting the crime of illegal business operation.